Baby boomers are coming to the realization that you can’t take it with you and are taking on more debt, which is in contrast to younger consumers, who are reducing their overall debt burdens.

The amount of debt held by people between the ages of 50 and 80 has increased by 60% during the past 12 years, according to data analyzed by the Federal Reserve Bank of New York.

One possible explanation for the increase in debt held by older Americans is the Great Recession, which started in 2008. Banks everywhere tightened their underwriting standards and decisively cut back on the amount of money they were lending. That made it harder for people, especially younger consumers, to get credit. Also, the study hypothesizes, is that banks may just be favoring older Americans in today’s economic climate.

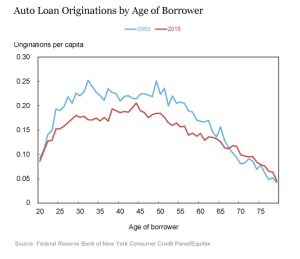

For auto loans, according to the data, more older consumers are buying cars than they did 12 years ago, coupled with fewer younger consumers purchasing new cars.

For auto loans, according to the data, more older consumers are buying cars than they did 12 years ago, coupled with fewer younger consumers purchasing new cars.

One good thing for financial institutions – and perhaps a bad thing for collection agencies – is that older people tend to have better credit performance than younger Americans. That means that older people are better at making their loan payments on time, which means fewer opportunities for collection agencies.

Also a contributing factor is that older Americans have higher credit score than younger consumers. Better credit scores make it more likely that a consumer will be approved for a loan application and more likely that payments will be made on time.

For collection agencies, this is a trend that bears further assessment. The tone and tenor of collection calls, letters, and other interactions should take into account the dynamic that older consumers are more likely to have more debt than younger consumers. Tailoring calls and communications to the right age demographic is a necessary component of an effective collections strategy.

Hence the aging of the American borrower bodes well for the stability of outstanding consumer loans. At the same time, the likely combination of muted credit access and lower demand for credit that we observe among our younger borrowers may well have consequences for growth. The graying of American debt that we observe between 2003 and 2015, then, might be interpreted as a shift toward greater balance sheet stability, and away from credit-fueled consumption growth.