The amount of outstanding credit card debt declined by more than $100 billion between 2019 and 2020, largely due to consumers paying down their debts, according to a report issued this week by the Consumer Financial Protection Bureau, which also detailed the pre- and post-chargeoff collection efforts and touted the rising usage of digital engagement tools like emails to collect on unpaid balances.

A copy of the report is accessible by clicking here.

For example, consumers receive, on average, between one and three phone calls per day, up to one voicemail per day, and two letters per month before credit card balances are charged off, according to the report. The report also contains analysis of debt sale trends, debt collection efforts during the COVID-19 pandemic, litigation trends, and recovery rates for third-party collectors.

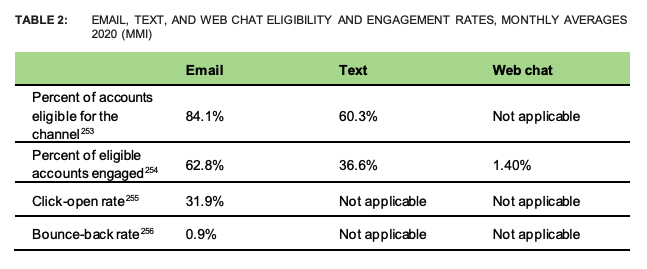

Issuers are pushing the use of digital communication tools, like email and text messaging, according to the report. Less than two-thirds of issuers said they were sending text messages to communicate with delinquent consumers when the CFPB surveyed them for the 2019 report. For the 2020 report, “almost all” respondents were using text messaging.

Interestingly enough, most credit card issuers “either prohibit or strictly limit” third-party agencies from attempting to communicate with consumers who have charged off debts using email and text messaging, unless the consumer specifically requests to be contacted via those channels.

The number of third-party collection agencies used by credit card issuers declined to 55 in 2020, from 62 in 2019, according to the report. The average third-party pre-chargeoff contingency fee for agencies was 15.7% in 2020, up slightly from 15.3% in 2018.

Fewer issuers continued to report using debt sales as part of their post-charge-off recovery strategies, according to the CFPB. Those who did sell portfolios reported selling about 5% of their post-charge-off inventory.