The Center for Responsible Lending, a non-profit consumer advocacy organization, has released a report about the impact of “abusive” debt collection practices in Oregon, saying that the state did not go far enough when it enacted a law that went into effect earlier this year.

The new law also requires debt buyers obtain a license when purchasing portfolios that include receivables from individuals in Oregon, makes changes to the items required when filing an initial pleading in attempt to sue an individual for an unpaid debt, and outlines a number of other practices that are now considered to be unlawful. There was some ambiguity in the law related to a lack of safe harbor language over validating debts, which was subsequently covered when the state legislature amended the law.

While Oregon’s new law requires debt buyers to include additional information about the debt and consumer in the initial court filing and to possess business records that establish the nature and amount of the debt, the new law does not require debt buyers to provide those “proof of debt” documents to the court. “Proof of debt” must be established by detailed information and original account-level documentation about the consumer and the debt. Critically, any future reforms requiring debt buyers to provide documentation of the debt and consumer to the court should clarify that affidavits are not sufficient to establish “proof of debt” unless accompanied by original account-level documents to support the claims made in the affidavits.

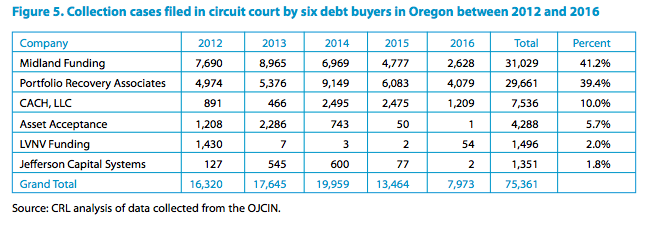

In conducting its analysis, the CRL looked at court records and filings between 2012 and 2016. The report noted that six companies were responsible for filing more than 75,000 lawsuits in the state, representing 25% of the total number of civil cases filed during that timeframe. Not one Oregon consumer won a lawsuit that was filed against him or her by a debt buyer, according to the report.

In conducting its analysis, the CRL looked at court records and filings between 2012 and 2016. The report noted that six companies were responsible for filing more than 75,000 lawsuits in the state, representing 25% of the total number of civil cases filed during that timeframe. Not one Oregon consumer won a lawsuit that was filed against him or her by a debt buyer, according to the report.

The report, however, makes some conclusions based on extrapolations or references to other reports or data provided by outside agencies.

For example, the CRL’s report notes data from the Federal Trade Commission that was released in 2013 which says that the name of the original creditor was provided on debts purchased by debt buyers only 46% of the time, and that the finance charges and fees were included only 37% of the time. So, the CRL’s report concludes that of the lawsuits filed by those six companies, “Oregonians owe as much as $18 million per year, in judgments for cases won by just six debt buyers that likely lacked sufficient documentation.” Using the phrase “likely lacked” is subjective and does nothing but attempt to paint an entire industry as bad using data that is more than five years old.

The report, however incendiary, is working. One Oregon newspaper published an article based on the report and used the headline:

New Report Shows Debt Buyers Are Choking Circuit Courts, Victimizing Oregonians

Debt collectors deploying “lawsuit factories” to collect on undocumented or improperly documented debits.

The report makes a number of recommendations. They are:

- Ensure debt buyers prove that the debt is owed

- Discourage debt buyers from acting as “lawsuit factories” by holding them accountable for initiating unwarranted legal actions

- Require that debt buyers substantiate their claims made during collection attempts

- Prohibit the collection of time-barred debts and other “zombie” debts