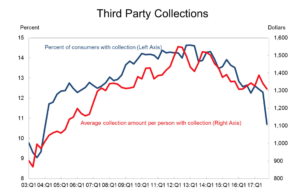

The number of individuals with a debt assigned to a third-party collection agency plummeted during the fourth quarter of 2017, while the average size of the debt in collections also decreased, according to data released yesterday by the Federal Reserve Bank of New York.

Just under 11% of individuals had a debt placed with a third-party agency, according to the report, down from more than 12% at the start of 2017. The average amount in collections dropped about $100, to just over $1,300 during the year.

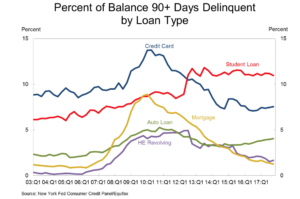

Delinquency rates on student loans tipped down in the fourth quarter from the third quarter, while delinquency rates on auto loans inched higher. On aggregate, about 4.7% of all debt was delinquent at the end of 2017. The total amount of debt, including mortgages, increased for the 14th consecutive quarter, and stood at $13.15 trillion. That is more than $473 billion higher than the previous record, set in the third quarter of 2008.

Delinquency rates on student loans tipped down in the fourth quarter from the third quarter, while delinquency rates on auto loans inched higher. On aggregate, about 4.7% of all debt was delinquent at the end of 2017. The total amount of debt, including mortgages, increased for the 14th consecutive quarter, and stood at $13.15 trillion. That is more than $473 billion higher than the previous record, set in the third quarter of 2008.

The report noted the flow of delinquencies from individuals who are less than 90 days behind on their bills to those who are more than 90 days behind increased in credit cards and auto loans.

“The flow into 90+ days delinquency for credit card balances has been increasing notably from the last year and the flow into 90+ days delinquency for auto loan balances has been slowly increasing since 2012,” according to the report.

“The flow into 90+ days delinquency for credit card balances has been increasing notably from the last year and the flow into 90+ days delinquency for auto loan balances has been slowly increasing since 2012,” according to the report.