Evidence suggests that there are more and more collection agencies that are opting not to report delinquencies to the credit bureaus because of the liabilities associated with posting information inaccurately, according to a number of sources.

There still does remain a cadre of agents who use credit reporting as an important tool to induce borrowers to make their payments.

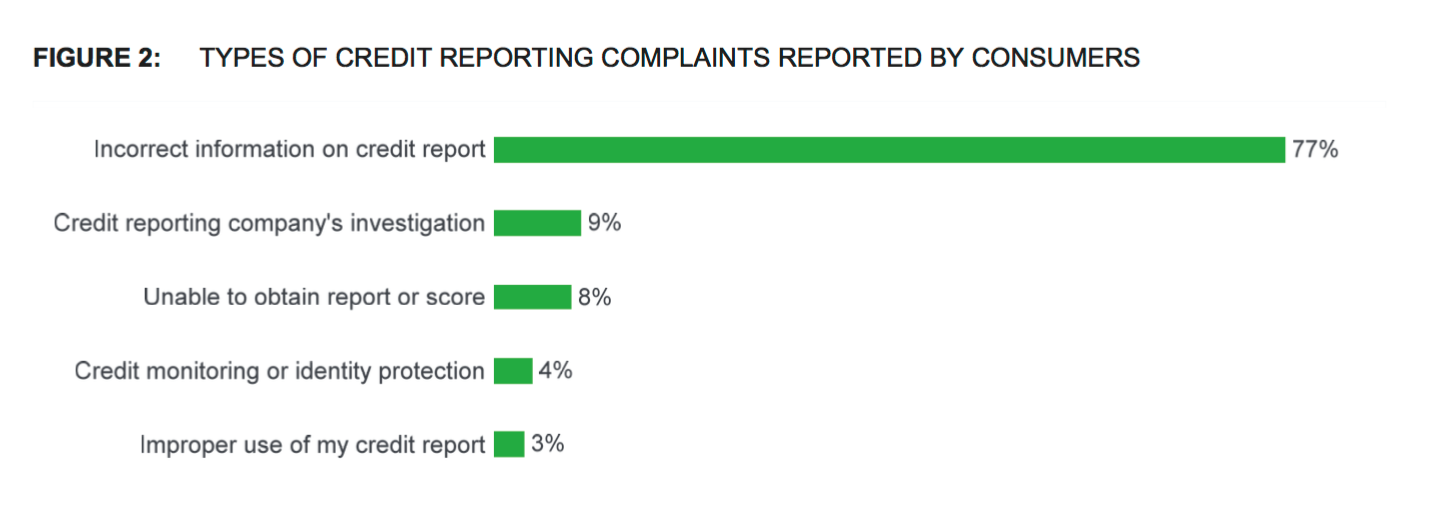

Inaccurate information on a credit report is one of the most complained about categories when consumers file complaints with the Consumer Financial Protection Bureau.

Consumers are filing more complaints about their credit reports, as well. Equifax, Experian, and TransUnion, the three major credit bureaus, were among the top four companies in which complaints were filed against, according to data released by the CFPB and credit reporting was the category with the highest month-over-month growth.

“I have clients who are just fed up,” said John Bedard, a partner in the Bedard Law Group. “They are saying they aren’t going to report to the credit bureaus, they are just going to sue,” consumers instead.

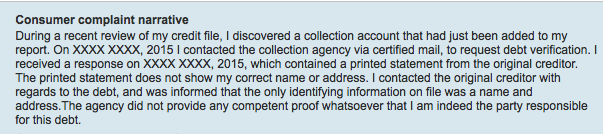

With more lawsuits being filed by plaintiffs attorneys representing consumers, the litigious air that surrounds the collections industry is enough to force many companies to re-think their policies and procedures. Here is an example of a complaint filed with the CFPB by a consumer regarding the appearance of a collection item on his or her credit report:

In many cases, collectors are subject to the whims of their clients in whether or not to report to credit bureaus. Some creditors want collection agencies to do it, others do not, and the rest leave it up to the agency to use its best judgment.

“I am old school and I am still in the mindset that a debt owed is a debt owed and needs to be paid,” said Dan Ramey with US Collections West in Phoenix. “The credit bureau reporting process is a strong force to assist in the collection stages for both creditor and collection agency.”

But Ramey admits that his company only reports to one credit bureau because it has the largest marketshare.

Whenever its clients allow, Simon’s Agency reports to the credit bureaus, said Tim Buckles. The agency tries to make contact for 90 days before reporting the delinquency to the credit bureaus. But when reporting. Simon’s follows strict protocols to ensure that the information is not mis-applied, Buckles said. For example, they make sure of a Social Security number and date of birth match when reporting information to a credit bureau.

“When other collection agencies stop reporting, it de-leverages their ability to collect,” Buckles said. “It’s something we’ve always done.”

Simon’s specializes in representing healthcare companies and there are many in that space that want to be the “softer, gentler” client, Buckles said. In many cases, there is an emotional attachment between the patient and the healthcare provider and that bond makes it more likely that the client will opt not to have Simon’s report the unpaid debts.

For collectors, using credit reporting as a tool to convince borrowers that resuming their payments is the optimal solution is perhaps no longer worth the risk.

“Every tool that collectors have to awfully collect legitimate debt is being taken away from them,” Bedard said. “It’s getting harder and hard for agencies and lawyers to collect.”

Excellent article.