The CFPB has categorized the outline of proposals into three main sections: the integrity of the information, communication practices, and consumer understanding. AccountsRecovery.net will provide summaries of each section.

INFORMATION INTEGRITY

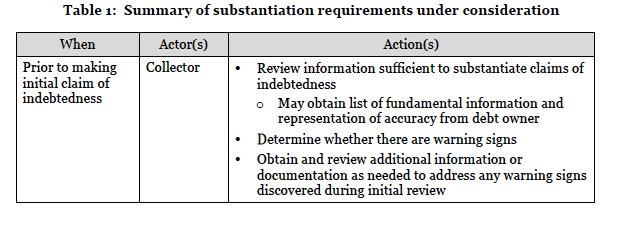

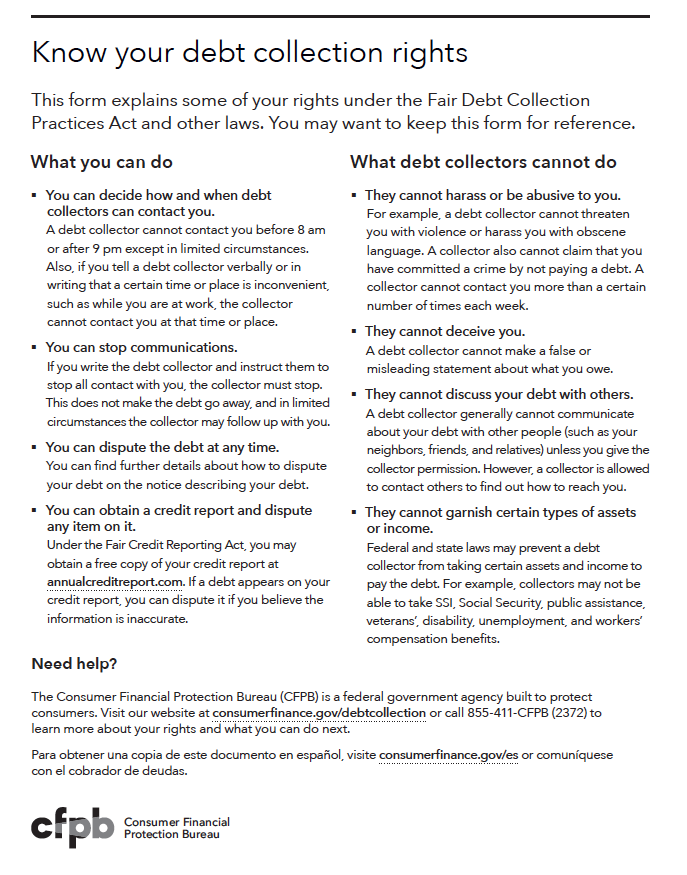

Collectors would be required to substantiate a claim that an individual owes on a certain debt.

The CFPB does not exactly lay out how a collector would substantiate a debt, offering that different debts and the “context surrounding collection” may require “flexibility” in making that determination. What it does say is that “the Bureau is considering identifying certain fundamental information that collectors can obtain and review that, along with a representation of accuracy from the creditor and a review for warning signs, would establish reasonable support for claims of indebtedness.”

The fundamental information, which can be included in a spreadsheet, could possibly include:

- The identity of the consumer

- The nature and amount of the debt

- The chain of title that provides the collector’s right to collect

Other information that may be required could include:

- The full name, last known address, and last known telephone number of the consumer

- The account number of the consumer with the debt owner at the time the account went into default

- The date of default, the amount owed at default, and the date and amount of any payment or credit applied after default

- Each charge for interest or fees imposed after default and the contractual or statutory source for such interest or fees

- The complete chain of title from the debt owner at the time of default to the collector.

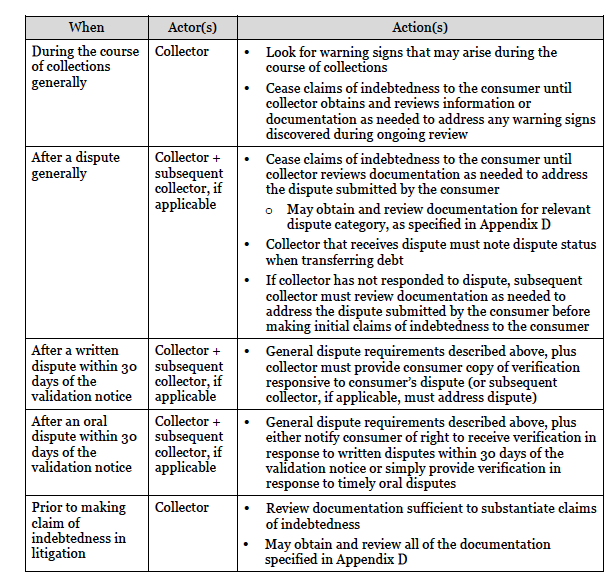

What constitutes a warning sign?

- Information for an individual debt is not in a clearly understandable form

- Information for an individual debt is facially implausible or contradictory

- A significant percentage of debt in the portfolio has missing or implausible information, either in absolute terms or relative to portfolios with comparable types of accounts

- A significant percentage of debt in the portfolio has unresolved disputes, either in absolute terms or relative to portfolios with comparable types of accounts.

The CFPB says it ruled out requiring collectors to review account-level information because it could be “overbroad” and “unduly burdensome.”

Collectors may also have to continue looking for warning signs while working an account and obtain more proof to verify a debt if a warning sign appears. Warning signs that may appear during the collections process include:

- A dispute filed by a consumer with respect to an individual debt

- The inability to obtain underlying documents in response to a dispute

- Receipt of disputes for a significant percentage of debt in the portfolio, either in absolute terms or relative to portfolios with comparable types of accounts.

The proposal would also define what a dispute actually is. A communication from a consumer would constitute a dispute

if they take the form of a question or challenge related to the validity of the debt (e.g., the amount of the debt or the identity of the alleged debtor) or the legal right of the collector to seek payment on the debt. Questions unrelated to the validity of the debt or the collector’s right to collect the debt would not constitute disputes. The proposed definition would not require consumers to use specific words to have a communication treated as a dispute.

The CFPB is also seeking to standardize how a collector verifies a debt if a consumer files a dispute within the initial 30-day window. For generic disputes, the following information would be required to validate the debt:

- The first and last name, address, and account number (with the creditor at the time of default) of the debtor

- The date of default and date of last payment

- The name and address of the creditor at default

- The amount of the debt balance at default and any post-default interest and fees, and a description of the amount owed.

For specific disputes, such as the individual claims to be the wrong customer, or the amount of the debt is incorrect, additional information would be required.

Here is a summary of the proposals:

When an account is transferred, either from one agency to another or if a debt buyer purchases a portfolio of accounts, the CFPB is considering proposals that the original and subsequent collectors would be required to follow.

Subsequent collectors would have to obtain and review information that could affect their obligations to comply with the FDCPA. That information includes:

- Whether the debt was disputed in writing within 30 days of receipt of the validation notice and either (1) a statement that the debt was verified; or (2) the details of the dispute, including information the consumer submitted or the prior collector provided

- Whether the debt was disputed orally or more than 30 days after receipt of the validation notice, and either (1) a statement that the claims were substantiated; or (2) the details of the dispute, including information the consumer submitted or the prior collector provided; o Any time, place, or method of communication that the consumer stated is inconvenient

- The name and address of any attorney who is representing the consumer in connection with the debt

- Whether the consumer’s employer prohibits the consumer from receiving collection communications at the place of employment

- Whether the collector has made confirmed consumer contact, and the contact information used to establish such contact

- Whether the collector has provided the time-barred debt disclosure

- Whether the consumer is deceased and, if so, the date of death

The CFPB would require similar compliance responsibilities with respect to other laws, such as the Servicemembers Civil Relief Act.

When a debt is bought or sold, additional information would have to be transferred to the subsequent collectors, including payments submitted by the consumer; bankruptcy discharge notices; identity theft reports; disputes; and any assertion or implication by the consumer that his or her income and assets are exempt under federal or state laws from a judgment creditor seeking garnishment.

VALIDATION NOTICES

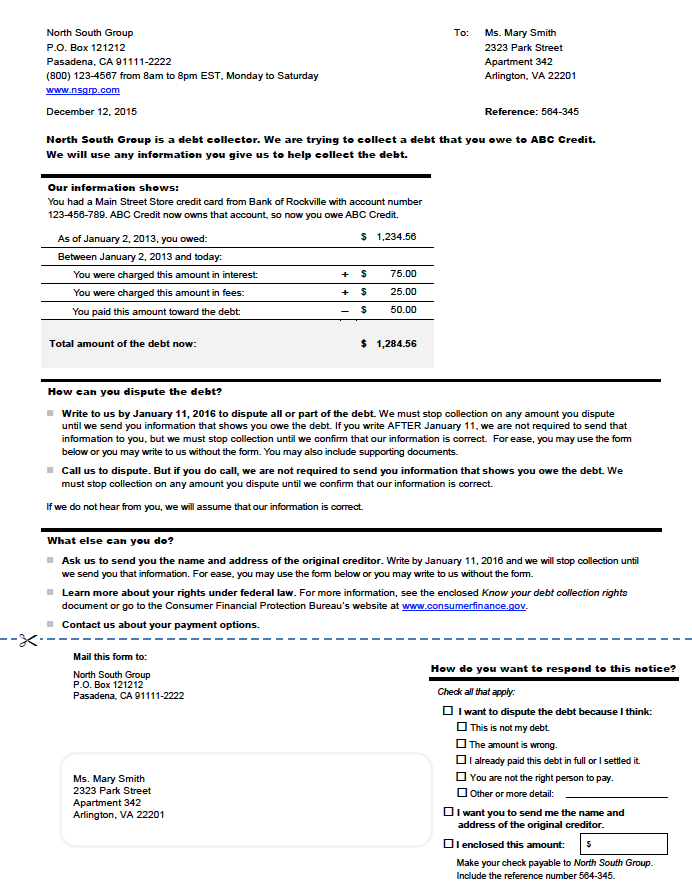

Collectors would also be required to change the content of their validation notices, under the proposal. The CFPB is considering adopting a standard validation notice, which would look something like this:

Collectors would also have to provide individuals with a “Statement of Rights” when sending a validation notice. That statement would look something like this:

Collectors would also be barred from reporting a debt to a credit bureau until the individual has been contacted and sent a validation notice.