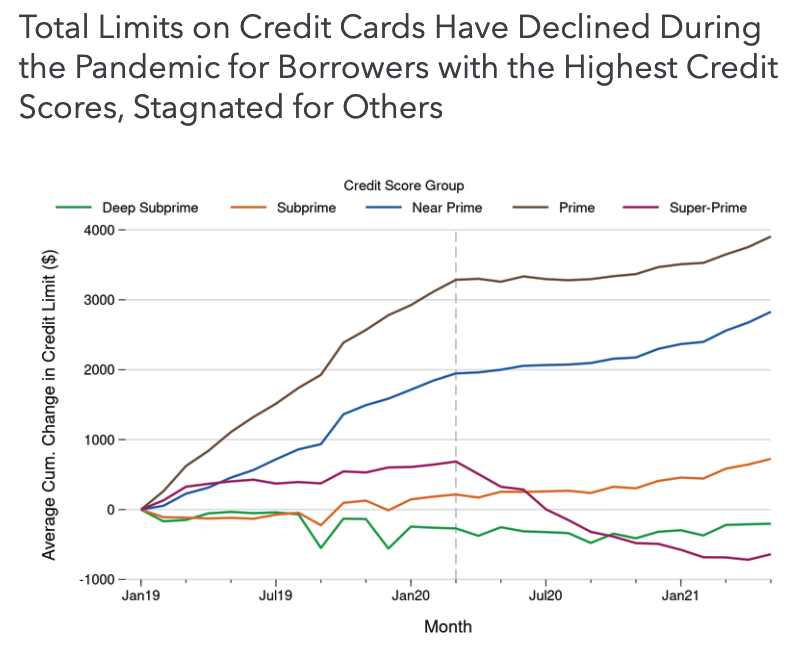

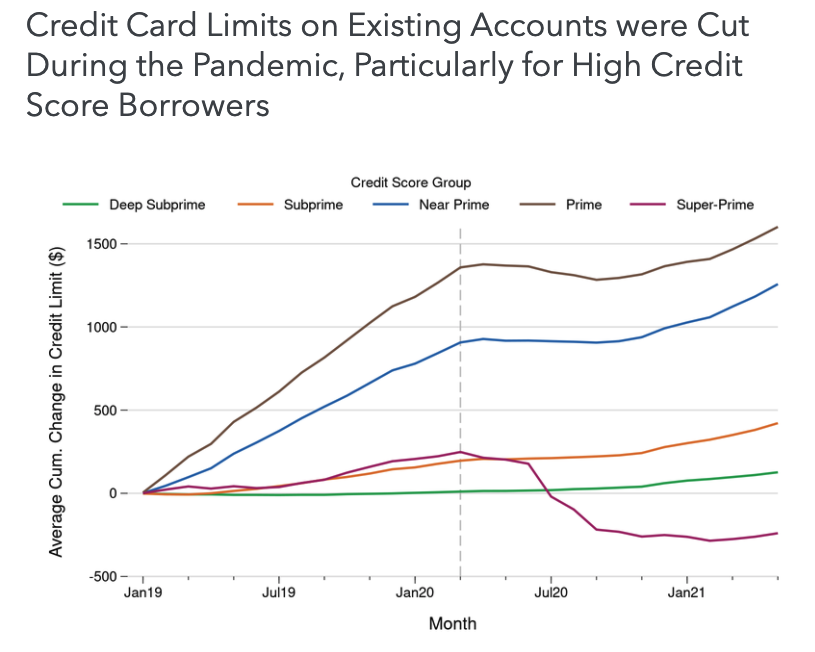

Credit card lenders and financial institutions are apparently a little leery of the state of the economy and consumer’s ability to meet their financial obligations and are keeping balance limits largely stationary for the time being, except for one group of consumers — and it’s probably not the group you would guess — according to data released this week by the Consumer Financial Protection Bureau.

In fact, consumers with the highest credit scores, referred to as “Super-Prime” have seen the balance limits on their credit cards slashed during the last 18 months, while the limits for consumers with Prime and Near-Prime credit scores have slowly increased, and the limits for consumers with Subprime and Deep Subprime credit scores have remained largely unchanged. The average credit card balance for a Super-Prime consumer has declined by more than $1,300 since the start of the COVID-19 pandemic in March 2020.

With limits not all moving in the same direction, it is likely a sign that lenders aren’t sure about how consumers are going to manage their finances for the foreseeable future, especially as they deal with the continued fallout of the COVID-19 pandemic, the end of additional unemployment benefits, and potential issues returning to work.

While the average change in credit card limits flattened out during the initial months of the pandemic, there are signs that in recent months, lenders have begun to loosen the reins and give consumers more credit with which to spend.

The report does not draw any inferences or conclusions based on the data that it published, but companies in the accounts receivable management industry would likely be well served to note the changes as they build their collection and propensity to pay scoring models for the remainder of 2021 and into 2022. Lower limits mean that consumers are more likely to use more of their credit availability, which increases their debt-to-income ratio and affects their credit score. That could lead to higher interest rates and debt payments moving forward. Credit card limit changes are also a sign of how banks think the economy is trending. They will generally loosen their lending guidelines when times are good and tighten them when the economy hits a rough patch. Seeing how they are adjusting credit card limits and whether they are allowing consumers to borrow more or less can offer insight into which direction financial institutions think the economy is moving.