Undoing a big split among the Circuit Courts of Appeals, the Third Circuit Court of Appeals yesterday overturned a well-known precedent and ruled that there is no written dispute requirement under Section 1692g(a)(3) of the Fair Debt Collection Practices Act.

A copy of the ruling in the en banc decision of Riccio v. Sentry Credit can be accessed by clicking here.

The Third Circuit now joins a number of other Appeals Courts that have ruled that disputes under Section 1692g(a)(3) can be made orally, as well as in writing.

The plaintiff had filed a class-action suit against the collection agency after she received a validation notice. The collection agency had used the language from Section 1692(g) of the Fair Debt Collection Practices Act in the validation notice.

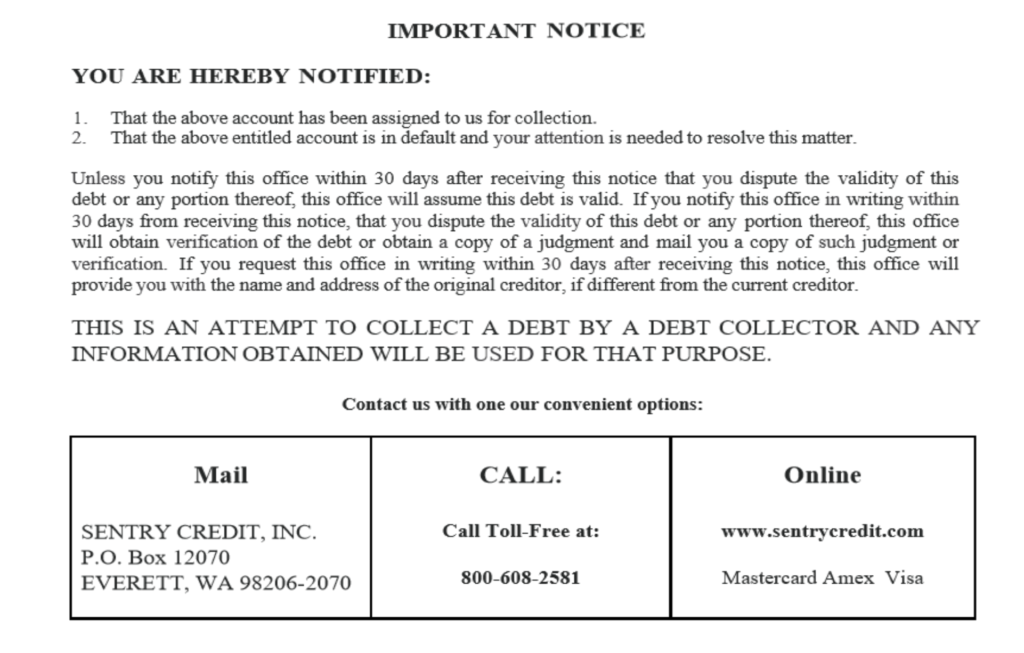

The plaintiff argued that the boxes offering different means of contacting the collection agency were confusing and did not make it clear that a dispute had to be filed in writing, even though it says “If you notify this office in writing within 30 days from receiving this notice…” in the text above the boxes.

A District Court judge granted the defendant’s motion for judgment on the pleadings, which the plaintiff appealed to the Third Circuit.

The issue at hand is what how a dispute may be filed under Section 1692g(a)(3) of the FDCPA, which states that the validation notice must include: a statement that unless the consumer, within thirty days after receipt of the notice, disputes the validity of the debt, or any portion thereof, the debt will be assumed to be valid by the debt collector. Other sections of 1692g specifically include the word “written,” whereas 1692g(a)(3) does not. Back in 1991, the Third Circuit, in Graziano v. Harrison, ruled that Section 1692g(a)(3) “must be read to require that a dispute, to be effective, must be in writing.”

Willing to admit it needed to look at the text with “fresh eyes,” as well as 30 years of rulings from other courts, the Third Circuit reversed itself. If Congress did not include the written dispute requirement in 1692g(a)(3) — a requirement that is specifically mentioned in other parts of the FDCPA — the Third Circuit determined it must trust that Congress knew what is was doing.

“By expressing our view today, we put an end to a circuit split and restore national uniformity to the meaning of §1692g,” the Appeals Court wrote.