More credit card debt is heading into delinquency status while debt on auto loans, mortgages and other types of household debts remain largely the same, according to data released today by the Federal Reserve Board of New York.

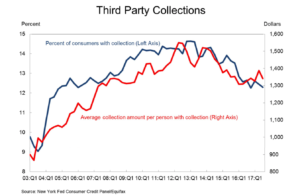

The number of people with debts placed with third-party collection agencies declined slightly, as did the average amount of debt in collection per person.

The number of people with debts placed with third-party collection agencies declined slightly, as did the average amount of debt in collection per person.

The total amount of household debt continued to set a new record, climbing for the 13th consecutive quarter. At the end of the third quarter, there was $12.96 trillion in outstanding debt in America, up $116 billion from the second quarter and $280 billion higher than the previous record, set during the third quarter of 2008.

What makes things more interesting is that the growth shows no sign of slowing down. Credit inquiries, an indicator of consumer demand, increased in the third quarter, compared with the second quarter. That means that there will likely be another increase in the amount of debt outstanding in the final three months of 2017.

More than 11% of the $1.36 trillion in outstanding student loan debt was seriously delinquent at the end of the third quarter, meaning that no payments had been received within the past 90 days. That amount was unchanged from the second quarter.

The number of new credit card accounts and auto loans continued their upward trend. In the case of credit cards, the number of accounts is close to the historical high set nearly a decade ago, while in the case of auto loans, a new record is being set every quarter.

The limits and balances on credit cards were also higher in the third quarter.

Credit cards appear to be a possible sore spot on the horizon, with the number of accounts transitioning from being current to being delinquent, and those from being delinquent to seriously delinquent both increasing. The increases were less pronounced in the other asset classes — mortgages, auto loans, and student loans.