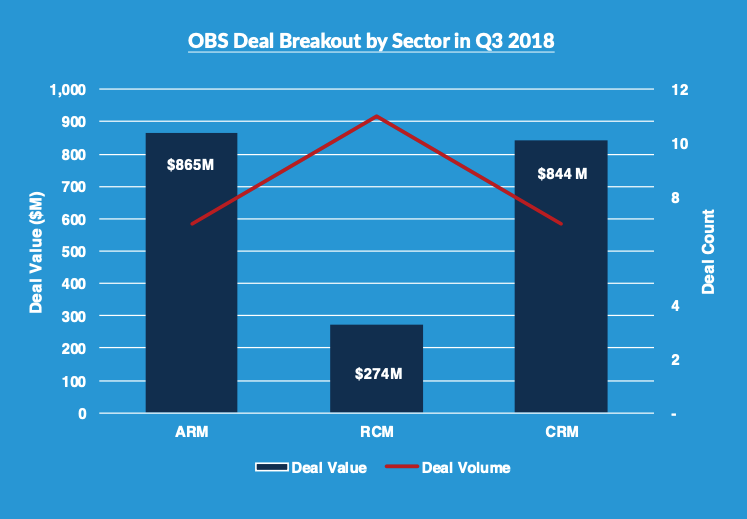

Following two straight quarters of at least $1 billion in merger & acquisition activity in the ARM industry — after only one $1 billion quarter in the preceding three years — there had to be a bit of a slowdown in dealmaking, which was the case, according to data released by Corporate Advisory Solutions. There were seven deals with a combined deal total of $865 million during the third quarter, down from 11 deals worth $1.16 billion in the second quarter.

Economic uncertainty and concerns over a recession sitting somewhere on the horizon may push delinquency and default rates higher, which could increase the interest from investors in purchasing collection agencies and debt buying firms, but that interest could be dampened by the pending debt collection rule from the Bureau of Consumer Financial Protection, depending on what is included in the proposal, due out by March 2019.

One piece of good news for the debt-buying industry, according to CAS: more creditors are “beginning to expand their vendor networks and are considering selling off accounts to debt purchasers,” the company wrote in its quarterly newsletter.

On the Revenue Cycle Management side, there were 11 deals with a total value of $274 million completed in the third quarter, compared with five deals worth $987 million in the second quarter. Collecting on unpaid bills continues to be a challenge for healthcare providers and more are looking to outsource that function to improve recovery rates, but at the same time, more facilities are looking to consolidate the number of RCM vendors they conduct business with, which means those companies need to expand their product offerings to be more competitive and attractive to potential clients.