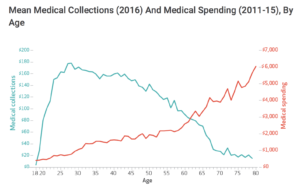

An interesting thing happens to people around the age of 62 or 63 years old, according to the results of a new study. While the amount of money spent on medical care is on the way up when individuals hit that age bracket, the amount of medical-related collections is actually on the way down, according to the study, which analyzed the credit reports of 4 million individuals.

In fact, the amount of medical debt in collections decreases steadily as individuals get older from the age of 25, according to the study, even though the amount of medical spending increases by a factor of 30 for individuals between the ages of 25 and 80.

In fact, the amount of medical debt in collections decreases steadily as individuals get older from the age of 25, according to the study, even though the amount of medical spending increases by a factor of 30 for individuals between the ages of 25 and 80.

The most likely explanation for why the amount of medical debt decreases while the amount of medical spending increases is the amount of health insurance individuals have as they get older, according to the researchers who published the study.

“Policies that promote insurance coverage for younger adults may have the greatest effect on reducing medical collections,” according to the authors of the study, which include economists from the Federal Reserve Board, the Bureau of Consumer Financial Protection, and the American Enterprise Institute. “However, because most medical debts are relatively modest in size, insurance plans with high deductibles might have only a limited impact. These findings are relevant to a host of policy considerations—particularly with regard to insurance design and regulation.”